Dream and Hustle

Creating a Peer to Peer Blockchain Hood Incident Coverage Platform

Thursday, February 15, 2018

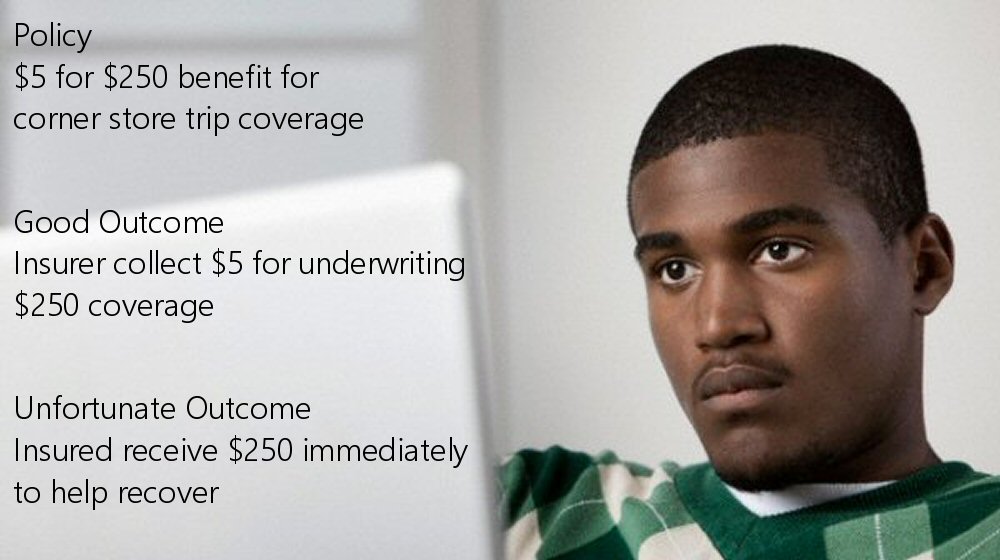

One of the biggest fear and concern in the black community is if something bad happen, it will be a devastating financial impact even just to pay deductibles or come up with money. A peer to peer blockchain coverage system can provide a solution and we cover the model in detail in this article.